Financial Modelling for Startups

Whether you are planning the next 1, 2, 5, or 10 years of your business, raising funds, or monitoring the financial health of your business, a well-built financial model is your go-to decision making tool. A financial model is a great tool to understand, plan, and manage any business idea. However, building a financial model can be overwhelming, especially for those who aren’t a finance-whiz.

Most startup founders are inundated with running and growing their venture, leaving them with very little time and motivation to make a financial model for their business. This often leads them to skip building the financial model altogether, using an off-the-shelf template from the internet, or putting some basic sales and expense figures in a spreadsheet, but none of these methods serve the purpose of a financial model.

Over the years of interacting with several startups and helping them build their financial model, we have learned that it is important for every startup, across the finance knowledge-curve, to understand why every startup must have a financial model and how to quickly build one that is suited for their business.

This is our comprehensive guide to building a financial model for startups. But anyone can use this guide to build a financial model for their business. Our guide answers the following questions

• What is Financial Modelling?

• Why do you need a financial model?

• How do you make a financial model?

What is Financial Modelling?

Financial modelling is an exercise done to assess the current financial position of the business, forecast its future financial performance, and estimate its value. Financial models help get an in-depth and objective understanding of a business based on certain numerical data and answer the big questions that entrepreneurs inevitably encounter

• How- & how much- will the business earn?

• How much money is needed to start/grow the business?

• When is the money needed?

• What is the value of the business?

Why do we need a financial model?

Understanding the Financials: The foundation of running a successful business requires having a sound understanding of its financial condition – Is the business making profits? What are the biggest expenses? How much money is needed to run the business? Who are the most profitable customers? And so on. To answer these questions, a financial model is used as it gives insights on all the financial transactions, both income and expenses, of the business in a structured format.

Budgeting Decision- Making decisions based on gut takes a business only so far. In reality, we need numbers and the hard truth they tell to make informed business decisions. The decision can be as small as purchasing pens & paper or as big as launching a new product - a wrong decision can make or break a business. A financial model shows the financial implications of a decision. Thus, helping to decide which tactic or strategy to go ahead and which to avoid.

Raising Funds – Every business, especially startups, need funds at different stages of its life cycle to run and grow it. Funds can be raised via varied sources - Investors, Lenders or Strategic partners. Most of these sources invest their money with the expectation of future financial gain. Some of the sources, such as strategic partners, also seek board positions while investing in startups. To decide whether to fund a startup, almost all investors want to see the financial model of the startup. This helps them understand the business, analyse the financial performance, determine the funding needs and estimate the potential value of the startup. Different investor value startups differently, which we will learn in the next section.

Sources of Funding

One of the primary purposes of a financial model for startups is to raise funds. Investors or funders differ based on the amount of money they invest, time horizon, type of funding, and stage of the startup during which they invest. Most importantly, these investors have different approaches to value a startup, and therefore, the complexity of the financial model also differs.

FRIENDS AND FAMILY: Friends and family members are usually the first types of investors, an entrepreneur pursues to raise funds. They generally invest for a short period of time and mostly invest in the idea/early stage of the startup, known as seed capital. These investors typically do not require a financial model to make their investment decision.

INCUBATORS AND ACCELERATORS: Incubators focus on innovation while accelerators concentrate more on helping scale the startup. These types of investors also invest mostly at idea/early stage with an investment horizon of two-three years. This category of investors uses a financial model to mainly assess the business concept, its growth potential, and how it can rapidly grow.

BANKS: Banks, traditionally give interest-bearing loans and do not invest in startups. However, as the startup grows, banks may offer it a line of credit and loans. Thus, banks require a financial model to assess the start-up’s ability to pay back the funds borrowed.

ANGEL INVESTORS: Angel investors are usually High Net-Worth Individuals (HNIs) who seek to invest in the early stages of startups. The stage of investment, amount invested, and investment horizon can differ - from a short period to pre-IPO stage. Most angel investors require a basic financial model and their method of valuing a startup can vary.

One of the most preferred valuation methods used by Angels is “The scorecard valuation method.” This method compares the startup with other similar funded startups and modifies the startup’s valuation based on factors such as region, market, and stage of business.

VENTURE CAPITAL/PRIVATE EQUITY (VC/PE): They are considered the holy grail of investors for most startups that seek funding. VCs/PEs invest mostly in the later stage of a startup intending to own a significant proportion of the business. Therefore, they make large investments and require a very detailed financial model.

FAMILY OFFICES: Family offices are private wealth management services that serve the financial and investment needs of wealthy families, which can comprise an individual, a single-family or multiple families. They usually invest in sectors in which they have expertise or in which they have a business. Their investment horizon can vary from short to long term.

CORPORATE INVESTORS: Corporations also invest in startups to diversify their investments and to add to their future growth. They typically invest with a long-term horizon, often acquire majority ownership. They require a financial model for similar reasons as most investors, to analyse the key parameters of the business, and to assess the synergy of the startup with the corporation.

So, until now we have learned…

• What is financial modelling?

• Why do we need it?

• Who all need a financial model?

Now let’s see what does a typical financial model consists…..

Key components of a financial model

Many believe that revenue and profitability estimations in the financial model are the keys to successfully attracting investors. The truth is that most sophisticated investors, primarily Venture Capital and Private Equity funds, make their own estimation and are more interested in the soundness and logic of the estimations. To do their calculations, investors want information on the assumptions, the structure of financial model, and the relationship between different components within the model. If the financial model passes these tests of investors, then it demonstrates that the entrepreneur has a strong understanding of the business.

Let’s get into discussing the different components that go into making a sound financial model that provides all the information required by entrepreneurs and investors.

Revenue Forecasting

The first step in building the financial model of an early-stage start-up is to estimate the revenue the startup is expected to earn from selling its good and services, usually calculated for the next five years. The revenue forecast is also used to develop a go-to-market strategy.

There are two popular ways to perform revenue forecasting.

I. Top-Down Approach

II. Bottom-up Approach

Top-Down Approach

The top-down approach starts from a macro perspective towards a micro view. We first calculate the total market size of the industry in which the business operates and then estimate the market share (proportion of total market) that the startup can serve.

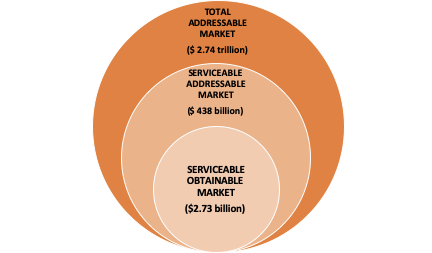

A useful method of doing top-down revenue forecasting is the TAM SAM SOM model:

a. TOTAL ADDRESSABLE MARKET (TAM) – The total addressable market, also known as the total available market, is the overall revenue opportunity for a given product or service in a year.

TAM = Average consumption (Quantity * Price) Per Customer Per Day * No. of Customers * 365 days

b. SERVICEABLE ADDRESSABLE MARKET (SAM) – SAM is a segment of the TAM which the business can serve. A segment can be based on various factors such as region, demography, psychographic, or behavioral.

SAM = Average consumption (Quantity * Price) Per Person Per Day* No. of Customers in Serviceable market * Number of days in a year

c. SERVICEABLE OBTAINABLE MARKET (SOM) – This is the proportion of SAM a business can achieve realistically in a specific time frame. Therefore, SOM represents the value of the market share the business aims to capture.

SOM = Average consumption (Quantity * Price) Per Person Per Day * (No. of customers in target market * % of market share) * Number of days in a year

Let’s understand the TAM SAM SOM method with an example:

Let’s say Jay, an aspiring entrepreneur, wants to sell coffee in India. What will be the TAM of his coffee business?

Assume,

- On average, a human being consumes 10gms of coffee every day

- The average price of 10gm of coffee is $1

TAM of the coffee business – Assuming the Population of the world is 7.5 billion

It is impossible for a company to achieve 100% of the TAM - unless it is a monopoly, has no geographical constraints, can service all types of users, has no regulatory restrictions, and has unlimited financial resources.

SAM of coffee business – Jay wants to sell coffee only in India (population of India is 1.2 billion)

SOM of coffee business - Jay estimates to sell coffee in 20 cities of India (population is 75 million) and capture 10% market share in the next five years.

Jay’s Coffee Business Revenue Model using Top-Down method

Bottom-up Approach

The second method is the bottom-up forecasting approach. In this method, begin by estimating the startup’s internal capabilities and work up to forecasting its revenue.

Let’s try to forecast the revenue of Jay’s coffee business using the bottom-up approach.

Jay wants to sell coffee in India across 20 cities over next five years.

• Average consumption per person – 10 grams

• Price of coffee - $1 per 10 grams

• *Achievable market share - 10%

TOTAL REVENUE FORECASTED / SOM - $2.73 BILLION (APPROX.)The bottom-up approach is less dependent on external factors, but its drawback is that it is based mostly on the Company’s internal capacity. The top-down approach also has some drawbacks, mainly the assumptions used to determine SOM. Therefore, we always recommend validating the forecasted revenue using the top-down and the bottom-up approach.

Also, the bottom-up approach is more helpful to forecast revenue for a short time period (1 to 2 years) while the top-down approach is more suitable for a more extended term period (3+ years).

After forecasting the revenue, the next step is to estimate all the expenses to be incurred to achieve the forecasted revenue.

Cost Estimation/Model

Expenses are the costs incurred for all the activities required to run and grow the startup. Various expenses are incurred by every startup, and this depends on the type and size of the startup’s business.

Let’s discuss the most common types of expenses incurred by startups.

Types of Expenses

1. Cost of Goods Sold (COGS)

2. Operating Expenses

o Selling, General and Administrative Expense (SG&A)

o Depreciation Expenses

o Research and Development Expense (R&D)

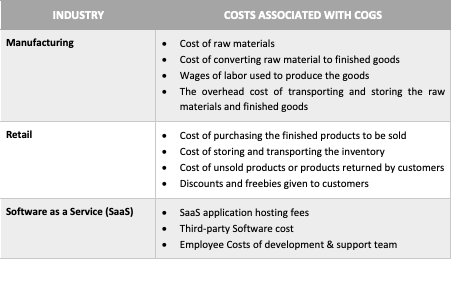

COST OF GOODS SOLD (COGS): Cost of Goods Sold (COGS) comprises the costs of all the activities required to produce a product or service, i.e. labor and material cost.

The costs that make up COGS vary depending on the type of business. Below is a table with examples of some of the major types of businesses and the costs classified as COGS.

Operating Expenses: These costs are incurred to support business activities but are not directly associated with the activity of producing products or services.

Operating Expenses are further categorised as:

- Selling, General and Administrative expense (SG&A)

- Depreciation expense

- Research and Development expense (R&D)

SG&A expense can be further divided into two parts:

a. Selling expense

b. General and Administrative expense

Selling expense: Selling expense consist of all the expenses which are directly or indirectly related to the sale of the products or services. These costs include advertising and promotions cost, transaction fee, sales commissions, and salaries of the sales team.

To estimate the selling expense, the cost of acquiring a customer (Customer Acquisition Cost), and the total revenue per customer (Customer Lifetime Value) must be calculated.

• CUSTOMER ACQUISITION COST (CAC): This is the amount of money the startup is willing to spend on acquiring each new customer. It tends to be higher for startups in their initial stages as they need to create their customer base from scratch, but it tapers down as the startup matures.

• CUSTOMER LIFETIME VALUE (LTV): This is the total profit a startup can expect to earn from a customer over the total life of the relationship with the customer. This is a valuable metric to determine the amount the startup should spend on customer acquisition.

General and Administrative expense: This consists of a variety of costs that a startup incurs in its day to day operations. These activities do not directly contribute to the production or sale of the goods or services but support the running of the business. Examples of such expenses are:

• Rent

• Utilities

• Payroll expenses

• Office supplies

• Accounting and legal expenses

II. DEPRECIATION EXPENSE

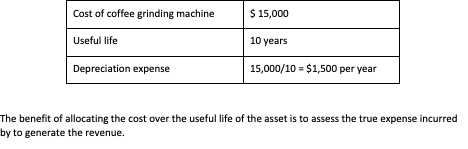

Depreciation expense is the total cost of an asset proportioned across its useful life. Although purchasing an asset is a one-time cost, it is used throughout its useful life to generate revenue, and therefore its one-time cost is also spread across its useful life.

There are different methods of calculating depreciation expense. A simplified process is to divide the total cost of the asset by the number of years it is considered useful.

Let us understand this through an example:

III. RESEARCH AND DEVELOPMENT COST (R&D)

R&D costs are the money the startup spends each year to develop new products and services or improve its existing ones.

PRO-FORMA / Financial Statements

Now we are getting to the heart of financial modelling. The three financial statements i.e. Profit and Loss Statement, Cash-flow Statement and Balance Sheet - summarise the financial transactions, depict the performance, and the current health of the business. These statements help investors and founders analyse the financial performance of the business.

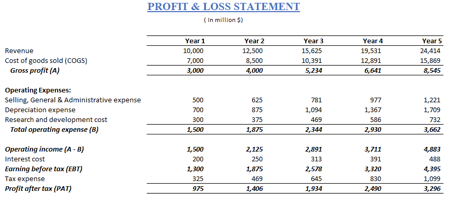

PROFIT AND LOSS STATEMENT (P&L): It is also referred to as the “Income Statement” or “Statement of earnings.” The P&L statement starts with reporting the revenue (top line) and subtracting the costs incurred in the business, and their difference is Profit (bottom-line). Thus, a P&L statement shows how much profit or loss was made by the business during a given period – year, quarter, month, etc.

The P&L statement is prepared on an accrual basis – income and expenses are taken for the activities that were done during the period under consideration rather than for those activities for which money was received or paid. For example, if a customer has taken possession of goods but is yet to pay for them, it will still be considered as revenue accrued, and thus the revenue will be taken in the P&L statement.

As a result, the profits shown in the P&L statement does not reflect the actual money earned by the business during that period.

Below is a sample P&L statement:

To understand the actual inflow and outflow of money (often referred to as cash), one needs to understand the link between the P&L statement and the Cash Flow statement.

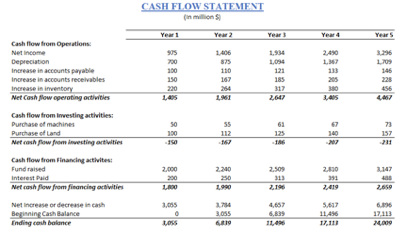

CASH FLOW STATEMENT: It provides a summary of cash received and spent during the reporting period, even if the activities for which the cash was used have not been done.

For example, if a customer has paid for the goods, but the goods have not yet been delivered to the customer, as the payment for the goods has been made, the revenue from the sale of goods will be considered in the Cash Flow Statement.

Thus, the CFS mentions the amount of money used during a given period and the amount of money available to the startup at a given point of time. It also allows investors and founders to assess how much cash is needed by the startup to run its operations.

The cash flow statement is divided into three parts

1. Cash flow from operating activities – It consists of all the inflows and outflows of cash related to only the main business activity of producing and selling its goods and services. This does not include cash received or spent on money raised for the business or on purchasing any assets, although these assets may be used for producing and selling goods and services.

• Cash received from customers

• Cash paid to employees

• Cash paid to suppliers for raw materials and services

2. Cash flow from investing activities – It consists of the inflows and outflows of cash for buying and selling assets, respectively. Examples of investing activities:

• Purchase of land, factories, and machines

• Investments & loans given to others

3. Cash flow from financing activities – It consists of the inflows and outflows of cash to finance the startup. Examples of financing activities:

• Funds raised by issuing shares (equity) of the startup

• Funds raised as loans (debt) from banks and other lenders

• Profits of the startup paid as dividends to Shareholders of the startup

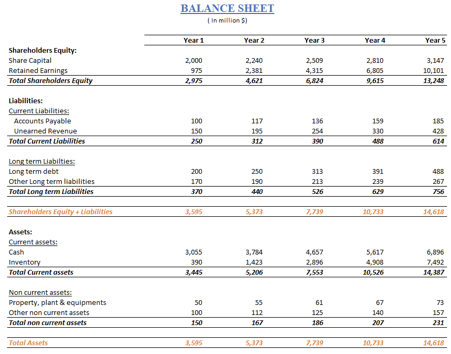

BALANCE SHEET : The balance sheet is a statement that reports everything a company owns (assets), everything it owes (liabilities), and the amount that belongs to the owners and investors (equity) at a given point of time.

• Assets: All the resources that the startup owns, such as money, machines, property, unsold goods, etc.

• Liabilities: The money that the startup owes to others such as loans, unpaid salaries, payments pending to suppliers, etc.

• Equity: Equity represents the shareholders’ (i.e., owners and investors) stake in the startup. It is the amount of money that would remain after selling all the assets and paying off all the liabilities.

Assets = Shareholders Equity + Liability

Now that we have understood how to estimate the revenue and expenses of the startup and summarise its financial information, it is crucial to test how these assumptions and estimates hold in the real-world. This is important to identify the weak spots and vulnerabilities of the business.

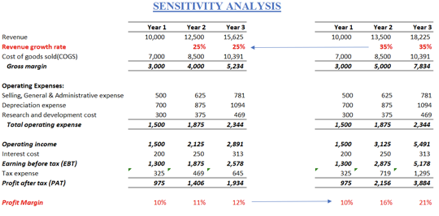

Sensitivity Analysis

In financial modelling, sensitivity analysis is testing different assumptions and their resultant impact on the financials of the startup. It is based on “what if” questions such as: What will be the effect on earnings if revenue changes by 10% rather than the current estimate of 15%? Sensitivity analysis helps investors and founders of the startup understand the sustainability of the business.

For instance, in the example below, the estimated growth rate of revenue is changed from 25% to 35%, increasing the profit margins. Thus, indicating how profit margins will change with increase in revenue. Similarly, we can change other estimates negatively and see its impact on the other variables.

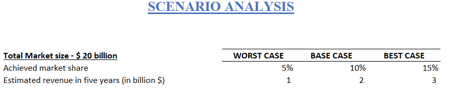

Scenario Analysis

Like sensitivity analysis, in scenario analysis, we create different versions of the financial model. In addition to the existing version, called the base-case scenario, we create best-case and worst-case scenario models based on extreme positive and negative external factors, respectively. These scenarios portray different results of revenue, expenses, and profitability. Based on these scenarios, investors and founders can take various informed decisions regarding funding, budgeting, etc.Let’s say that total addressable market for our business is $20 billion, and we estimated to achieve 10% of the market within the next five years as our base case. We can create scenarios in which we achieve 5% market share (worst case) or a scenario in which we achieve 15% market share (best case scenario).

Both sensitivity and scenario analysis help investors & founders determine the risks associated with the business and accordingly make informed decisions on the level of risk they want to take proportionate to the potential gains.

Financing

As we discussed earlier, one of the primary reasons for financial modeling is for startups to raise funds from investors. There are two main types of funding through which a startup can raise funds.

DEBT: When a startup borrows money from lenders as a loan, which it needs to be payback, is called debt financing. The loan is usually for a defined period and interest is paid to the investor as compensation for borrowing the money.

A key reason for a startup to raise funds through debt is that its existing shareholders do not have to give away a part of their ownership in exchange for the funds.

But raising funds through debt has some limitations too. For instance, if a startup raises funds through debt to build a SaaS product, which takes approximately two years to make, it will not have any positive cash flow from its operations for at least a few years to pay the interest on the debt. Instead, it will have to dip into its existing pool of money to pay the interest which it could have used for building the product.

Thus, it is advisable to raise funds through debt when the startup is generating enough money to pay the interest.

EQUITY: Equity represents ownership in a company and is in the form of shares, and each share represents a proportion of ownership (i.e. equity) in the startup. It is more common among startups to raise funds through equity rather than debt.

A startup can raise funds through equity by selling its shares to investors in exchange for money. The proportion of ownership it sells depends upon the valuation (which we will discuss in the next section) of the startup at the time of funding.

The main difference between raising funds through equity and debt is that

- In equity funding, the investors take the risk if the startup fails to make money but also share the profits

- In debt funding, the risk remains with the owners and not the lenders as the startup must pay back the funds taken to the lenders, irrespective of the amount of profit or loss the startup makes.

Valuation

Let us assume that a startup decides to raise funds through equity. Then the question arises - What percentage of the startup will have to be sold to raise a given amount of money? In order to do this, the value of the startup needs to be calculated.

Valuation is a process in the financial model to estimate the value of a startup. In a continually evolving world of business and finance, different people value startups differently. Now and then, valuation geeks come up with different methodologies to value a startup. Let’s discuss the traditional methods first...

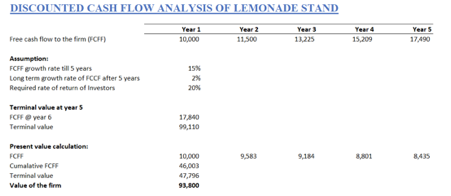

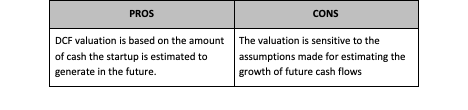

DISCOUNTED CASH FLOW METHOD (DCF): Discounted cash flow method is the most popular method of valuing a startup. In the DCF method, the value of a startup is estimated to be the present value of the money (cash flow). It is estimated to generate over a given period. Cash flows are the money available to shareholders after all the expenses are paid.

Let’s try to understand DCF valuation through an example:

A lemonade stand generates cash profit over the next five years, as given in the table below.

The sum of the present value of each year's cash profit is $ 46,003, discounted at a rate of 20%. The discount rate (20%) taken is the investors required rate of return.

The terminal value of the lemonade stand is calculated as $99,110 which represents the value of the firm at year 5. The present value of the terminal value discounted at (20%) turns out to be $47,796.

Total estimated value of the lemonade stand – Present value of cash profit of 5 years + Present value of terminal value

i.e. 46,003 + 47,796 = $ 93,800 approximately.

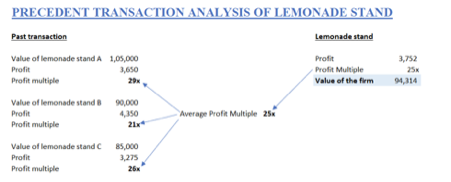

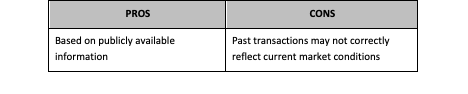

1. COMPARABLE TRANSACTIONS METHOD (COMPS): This method calculates the value of a startup using indicators (also called multiples) of similar sized startups from the same industry. This method assumes that similar startups have similar valuation multiples.

Some of the multiples that are a good proxy to determine the value of a startup:

1. Price/Earnings ratio

2. Monthly Recurring Revenue (SaaS business)

3. Number of outlets (Retail business)

4. Number of users (customers)

Let’s take the same example of a lemonade stand and value it using comparable company analysis method.

- Lemonade stand profits in the latest financial year: of $3,752

- Price/Earnings ratio of publicly listed lemonade business: 25x

Thus, the value of the lemonade stand will be $3,752 * 25 = $ 93,800

A financial model does not necessarily have to comprise all the components mentioned in this guide, but it is essential to have all these components when pitching your startup to potential investors.

Conclusion

After going through this guide, we hope it has given you a good understanding of financial modeling and convinced you that it is essential for your startup to have a financial model.

Do remember that financial models are not one-size fits all! Each startup is unique based on its sector, its customers, its business model, the market conditions, and many more factors. Thus, the smallest of incorrect inputs can render its financial model inapplicable.

A robust financial model must reflect the uniqueness of the business solution and potential value of the startup, especially to potential investors.